Criminals don’t play by the rules and often embrace new technology to exploit gaps in control environments. That’s why they’re able to reap massive profits from fraud and money laundering operations. In their efforts to thwart money laundering and other criminal activities, many financial institutions (FIs) will find their anti-money laundering (AML) programmatic capabilities limited by antiquated legacy systems, many of which are solely rules-based. It’s time for banks and other financial services providers to upgrade their AML programs and embrace machine learning models to augment their existing rules-based approach.

The Truth About Money Laundering

While the phrase “money laundering” has an exotic, exciting edge to it thanks in no small part to Hollywood mobster movies and international espionage thrillers, the truth is far less appealing than its glitzy big or small screen portrayals.

Money laundering activities trap an estimated 40.3 million people in slavery globally, fuel political unrest, and finance terrorism.

Considering the consequences, it’s no wonder governments enact AML regulations. These regulations have honorable and important intentions, but there’s no denying the ever-evolving compliance headaches they create for financial institutions.

What’s more, despite these regulations, money laundering continues to soar — in part because of technology. Per the United Nations on Drugs and Crime, advances in technology and communications have created “a perpetually operating global system in which “megabyte money” (i.e., money in the form of symbols on computer screens) can move anywhere in the world with speed and ease…The estimated amount of money laundered globally in one year is 2 – 5% of global GDP, or $800 billion – $2 trillion in current US dollars.”

What can be done? How can FIs avoid the repercussions of ineffective AML solutions and actually make an impact fighting financial crime? What’s more, how can banks accomplish this for today, along with the unknown financial crime schemes of the future?

Machine learning is a good start.

Machine Learning: AML for Today and Tomorrow

Machine learning is the cornerstone of state-of-the-art AML solutions both today and for the future of money laundering surveillance. It creates more efficient and effective teams by automating case enrichment and prioritization for investigators. Automation significantly decreases the number of false positives generated, which means teams don’t waste time on meaningless alerts. It also allows for more accurate risk scoring. According to ACAMS, “In one instance, a bank reduced the time (taken to work alerts) from several weeks to a few seconds.”

Rules-Only vs. Rules with Machine Learning Models

Legacy AML systems tend to provide high-volume, low-value alerts because they run on engines that only use rules. The overwhelming amount of false positives a rules-based system creates is akin to crying wolf. Depending on the size of the bank, analysts investigate around 20-30 false-positive alerts a day. Unless you have unlimited resources to review alerts, you’ll want a different strategy. Substantial fines — not to mention the media attention that goes with them — have been levied on institutions for failing to devote sufficient resources to review high-value alerts generated by automated AML systems.

AML programs powered by machine learning often utilize both rules and models, not just rules. Using both rules and models dramatically reduces false positives, increases operational efficiency, and requires less maintenance. Ultimately, this decreases the chances of getting fined and makes it harder for bad actors to guess the limits of the rules and sneak “just under the line.”

To help understand why running rules and machine learning models together is so effective, let’s discuss how rules and models-based approaches work for AML programs.

How rules-based risk engines work

Rules-based risk engines work by using a set of mathematical conditions to determine what decisions to make. It works like this:

- If an account shows more than $10,000 in cash transactions in 14 days, raise an alert.

One of the significant pros of using an advanced rules-based engine is that analysts can quickly create and implement new rules. Note that this isn’t true for all systems, only the more robust and innovative ones. The advantage is a clear rule with specific calculations, making it easier to demonstrate to regulators why and when the system flagged the event as suspicious activity.

But rules alone aren’t sufficient because they have too many limitations. They’re often too complicated to understand context and dive deeper than formulas. They also have fixed thresholds that criminals understand and purposely avoid, only YES/NO scenarios, produce too many false positives, require a great deal of manual effort to maintain, and have trouble detecting relationships between transactions — to name a few issues.

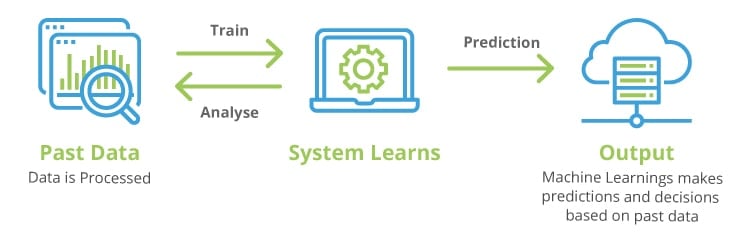

How machine learning risk engines work

Machine learning for AML strengthens rules with models, which further helps reduce high-volume, low-value alerts. That’s because machine learning models are trained with algorithms based on historical data to predict future behavior. Models work like this:

- Data science teams feed the machine massive amounts of historical data about known and suspected money laundering cases.

- Machine learning algorithms use the insights from these datasets to create statistical models, not deterministic rules.

- The machine learns what money laundering has looked like in the past and, equally important, what normal behavior looks like as well.

- The machine predicts the risk of money laundering based on known and suspected money laundering cases or by referencing cases that were reported to the regulator.

One of the benefits machine learning brings to the table is the ability to learn and adapt continuously. However, it’s important to note that machine learning models are only as good as the training data you feed them. It’s a bit circular but correct to say: if you can’t provide good, labeled training data to learn from, the machine can’t learn. That’s why it’s important to make sure your data sources use proper labeling practices.

Before getting started with supervised machine learning models, FIs would do well to assess potential impacts to controls, operational processes, and team structure. Once your team grows comfortable and confident in the supervised model’s performance and regulators indicate they are satisfied with how the current controls are performing, your organization can consider shifting to unsupervised machine learning models. These can detect behaviors that are wildly different from normal patterns. Having a small alert budget for these incidents l enables teams to explore a completely different set of transactions that would otherwise go undetected by rules.

Also, machine learning models take time to, well, learn. That makes them slower to implement. Once they are deployed, however, newer machine learning platforms provide an integrated feedback loop that allows some model algorithms to learn continuously from new data (like deep learning). Even if continuous learning is not possible and a periodic retrain is needed, models capture both good and bad patterns better than a set of rules (or a human) ever could. The result is criminals have a harder time deceiving the system by simply altering their behavior. This translates into smaller maintenance and monitoring time investments to keep up with evolving behaviors in financial crime.

So while it takes a bit more time to deploy, machine learning makes up for that time by providing more accurate alerts. Not to mention, ML saves your data science team countless hours they would have otherwise spent building and adjusting thousands of rules.

Criminals are always looking to exploit loopholes to their advantage. Instead of catching up with their latest tactics, banks have the opportunity to learn their tricks in real-time and bring illicit activities to light.

Ready to learn more? Download How to Choose a Machine Learning Platform to Detect and Prevent Financial Crime.

Share this article:

Related Posts

0 Comments10 Minutes

Boost the ESG Social Pillar with Responsible AI

Tackling fraud and financial crime demands more than traditional methods; it requires the…

0 Comments8 Minutes

Enhancing AI Model Risk Governance with Feedzai

Artificial intelligence (AI) and machine learning are pivotal in helping banks and…

0 Comments14 Minutes

What Recent AI Regulation Proposals Get Right

In a groundbreaking development, 28 nations, led by the UK and joined by the US, EU, and…